Industry Insight

Climate Tech’s New Trends and Growing Opportunities

Hundreds of entrepreneurs, investors, policy experts and climate activists attended IVP’s happy hour at SF Climate Week, an inaugural event that brought together thousands of people. If that’s not a strong signal that interest in climate tech is growing, follow the money: during the previous three years, investors have allocated nearly $100 billion to climate companies.

We’ve been exploring the climate landscape to understand what is driving all this activity. Climate tech is not new; it had a similar rise in interest in the 2000s, when it was known as cleantech, but that was considered mostly a failure. Back then, the alternative energy sources weren’t economically or technologically viable to win the market.

Today’s interest in climate tech is accelerating because of a much clearer, more compelling “why now” argument. Below, I highlight key trends, including:

- regulatory changes and government support

- improvements in technology reducing costs

- bottoms up, social commitment to sustainability

The ultimate goal of climate tech is to reduce greenhouse emissions. Many of climate tech’s biggest winners will include hardware and businesses with moats strengthened by physical products or proprietary technology in energy, land use and transportation. Some of the largest venture-backed companies in the space, including Tesla, Redwood Materials and Aurora Solar, illustrate this dynamic.

But at IVP, we also believe software and asset-lite companies can see significant success in climate and sustainability markets. Organizations and consumers are changing the way they work and live, and there are several areas where software makes sense because of the combination of changes in behaviors and physical technologies that are primed for optimization.

This is not unlike technology platform shifts of the past. In the development of the personal computer, the hardware advancements in processing power and memory laid the groundwork for the software revolution that followed. Through iterations between hardware, software and behavior change of consumers and organizations, we see exciting themes emerging in:

- decarbonization software

- vertical software

- applications/platforms that enable conscious consumers

Below are some of the key trends in climate tech and areas where we see opportunities.

Trend: Regulatory pressure, especially in the EU, is driving enterprise adoption of climate tech

The EU has made a goal of reaching net-zero greenhouse gas emissions by 2050. As the first step to that goal, it has mandated that nearly 50,000 companies begin disclosing emissions by 2024. To achieve that, those companies will have to start tracking and offsetting their emissions in the medium term and eventually change the way they operate.

By 2025, these reporting requirements will require companies to track not only emissions made by the companies themselves but also emissions across the companies’ entire value chain. Gathering the data to effectively measure an organization’s carbon footprint is a complex and time-consuming manual process that is ripe for automation disruption.

Emissions reporting is likely to become a requirement for U.S. companies as well. The federal Securities and Exchange Commission has proposed a regulation that would require publicly traded companies to disclose emissions.

Governments are also putting capital into accelerating the development and adoption of climate tech. The US Inflation Reduction Act allocates over $370 billion for climate initiatives, for instance, while the EU Green Deal Investment Plan proposes to dedicate up to €1 trillion to accelerate adoption of new energies and climate technology.

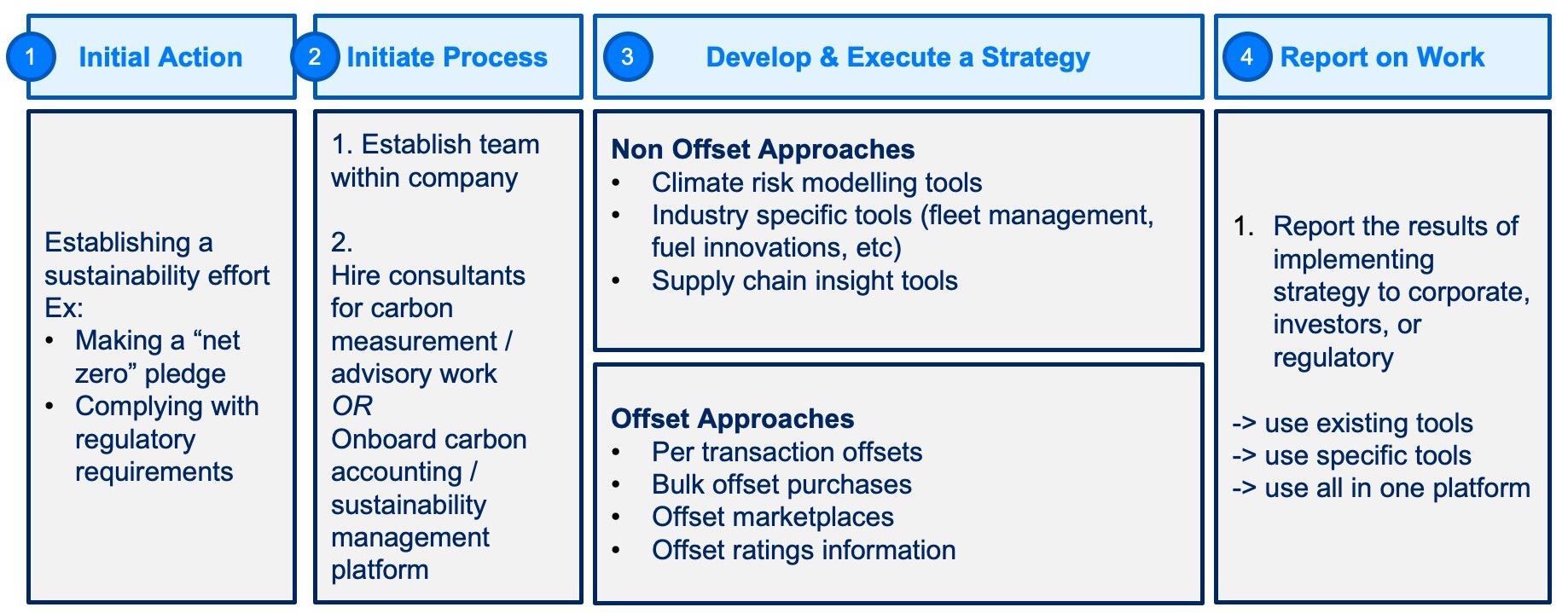

Opportunity: Decarbonization software for enterprises

The more climate and emissions data that businesses are required to collect, the greater will their need become for software to optimize for climate-conscious business decisions. The day is coming when enterprises will need to "climate plan" as a regular part of enterprise resource planning (ERP).

Companies like Watershed, Sweep and CarbonChain are allowing companies to track and measure their carbon footprint (see step 2 in the chart below). Once companies track their emissions, they’ll need to reduce or remove their carbon in various ways (see Step 3 below) – currently, the most prevalent method is carbon offsetting. Companies like Patch and Pachama are building software marketplaces to enable buying carbon credits; Sylvera is building software-based verification mechanisms to verify and rate new types of projects.

Trend: Technology has improved, and energy alternatives are reaching cost parity with fossil fuels

Adopting climate friendlier solutions is starting to become a smart business choice, allowing organizations to lower costs and reduce their environmental impact.

One of the biggest failures of the cleantech boom of the early 2000s was a reliance on energy alternatives that weren’t yet economically viable. That’s changed. Wind, solar and other alternative energy sources have now reached cost parity with fossil fuels.

Similarly, the total cost of owning an electric vehicle will soon be about the same as owning a gas vehicle, as the result of decreases in cost production and government incentives.

Opportunity: Vertical software for new and evolving markets

As costs of climate friendly technology decrease, tools to enable adoption will be important in all types of verticals, like in transportation, agriculture and commerce. California – the only U.S. state allowed to make its own auto emissions regulations – recently mandated that all new light- and medium-duty vehicles sold in the state must be zero emission vehicles (ZEVs) by 2035.

The anticipated growth of battery-powered cars will have all kinds of rippled effects, one being the massive toll on an aging American power grid. New technology companies will emerge to prevent the grid from reaching a catastrophic tipping point. Weavegrid, for example, builds software that optimizes energy consumption by tracking electricity-usage hotspots.

As massive wildfires and other climate-related impacts of global warming become more prevalent, vertical companies like Pano AI are helping fire professionals and homeowners protect against risk. In agriculture, vertical tools like FarmInsect are helping farmers access cheaper, more sustainable feed for livestock.

Trend: Younger consumers are driving greater commitment to decarbonization and sustainability

More than any previous generations, young millennials and Gen Z are demanding transparency and choice in climate-conscious goods and services. Consider the influence they’ve had in making organizations more accountable to lasting sustainability goals.

The majority of Gen Z shoppers prefer sustainable brands and are even willing to spend more for eco-friendly products or choose to buy second hand. In fact, resale is one of the fastest growing markets in retail, growing 10x+ faster than regular retail in the next few years. As impacts of climate change are becoming more apparent, young consumers are increasingly feeling urgency, and climate sustainability is among their priorities.

Opportunity: Platforms enabling sustainability conscious consumers

We’re excited by a growing ecosystem of new marketplaces and commerce tools that enable sustainable goods and fashion. For example, Archive allows brands to build a secondhand market into their business.

As their behavior changes, consumers want to know the impact they are making on the environment so they can make more climate conscious choices. Companies like Wren and Joro are allowing consumers to measure their personal climate footprint.

Ultimately, the path to a more sustainable future will require a diverse range of solutions and the commitment of collaboration between enterprises, consumers and governments.

Takeaways

Interest in climate tech is growing, with nearly $100B invested in the past 3 years

Climate tech software opportunities are accelerating due to clearer, more compelling reasons to act

Key trends driving activity include regulatory changes, technology improvements, and social commitment to sustainability

Decarbonization software for enterprises is an opportunity for automation disruption

Vertical software for new and evolving markets, such as transportation and agriculture, is another opportunity

Platforms enabling sustainability-conscious consumers are also emerging as a growing ecosystem

If you’re building in one of these areas, we'd like to hear from you!